Top Investment

Smart Investment Starts with Smart Strategies

As an independent investment planner, we have no ties to proprietary products. That means we can utilize any portfolio to help you achieve your goals. After all, investments themselves are tools – it’s how we package investments together that makes them successful.

Using data visualization software, we show you a holistic picture of your current assets. From there, we work to develop a strong understanding of your income needs and identify effective strategies to grow your wealth and minimize your tax burden.

We became a well-respected investment management firm because we look out for our clients and ensure that their successful and comfortable future is our focus.

Why Choose The Tranel Financial Group for Investment Management?

The Tranel Financial Group is an experienced investment management firm in Chicago. With our proficiency and commitment to tailored investment strategies, we bridge the knowledge gap of our clients to achieve their financial goals and build lasting wealth. Whether you’re planning for retirement, saving for education, or seeking to grow your assets, we provide personalized guidance every step of the way.

As a financial advisor, we offer independent advice that puts your interests first. We understand the complexities of financial management in Chicago and provide the insights and tools necessary to navigate today’s dynamic markets.

Watch our Investment Policy Video

Investments as Unique as Our approach

We can’t control fluctuation, but we can control the income potential of your portfolio. Our investment strategy is built with the goal of increasing the income potential of your portfolio. Markets can fluctuate, just like your personal circumstances, so don’t lose sleep over change.

The majority of the companies we invest with have above-average dividend growth. Across all of our models, we invest in 70 unique individual equity positions and 59 of those 70 positions have increased their dividend. None have decreased. Even when markets/investment allocations are down, the income power of their portfolio is up. By reinvesting a strong and ever-increasing dividend, you own more shares, and those shares are paying out more in dividends, whether the account value is up, down or sideways. **Past performance does not assure future performance.

Our investment strategies have helped people of Chicago make informed decisions. We focus on your needs and your growth, providing you with the most ideal outcomes for your future.

Our Investment Management Philosophy

Tailored Strategies for Every Client

Your financial situation is unique, and your investment strategy should reflect that. We offer customized investment management solutions, designed to meet your specific financial objectives. Our personalized approach means we carefully consider your financial goals, risk tolerance, and timeline to develop an investment strategy that’s right for you.

Holistic Approach to Asset Allocation

At The Tranel Financial Group, we believe in a holistic approach to asset allocation. Considering your financial situation, we develop investment strategies that optimize growth while managing risk. Our goal is to make every dollar work toward securing your financial future.

Active Portfolio Management

We employ active portfolio management techniques, constantly monitoring market trends and economic conditions. We strategically adjust your portfolio to optimize returns while minimizing risk. Our team of investment management professionals help your investments align with current market conditions.

Long-Term Perspective

We are committed to long-term investment success, avoiding short-term speculation. Our approach focuses on building a sustainable investment strategy that will serve your needs today, tomorrow, and in the future. Whether you want your wealth to grow or preserve it, we prioritize consistency and stability.

Watch our Asset Allocation Video

We Strive to Find That Perfect Balance of Risk and Reward

When markets are up, it’s human nature to want to capture upside and when markets are down, you want to capture as little of the downside as possible. Conservative allocations generally aim to reduce exposure to market volatility and may limit potential for higher returns. Conversely higher-volatility allocations generally aim for greater growth potential, but they may also experience significant declines during market downturns. A capture ratio measures how an allocation performs overall in up and down markets.

Equity-focused portfolios offer upside capture ratios when markets are strong. Our focus on recession-resistant sectors, quality dividends, and dividend growth rates may allow our allocations to enjoy less downside capture when markets are weak.

Watch our Financial Planning Video

Wealth Preservation and Growth

Two Crucial Components of a Retirement Investment Strategy

You only retire once. So when cracking open your nest egg, you have one chance to do it right. If you make a mistake, you likely won’t know until 10 or 15 years down the road. And then it’s too late. The most common mistake? Retirees treat their nest egg as one lump sum of money. There are costly pitfalls with investing, managing, and thinking about your money in this manner.

For example:

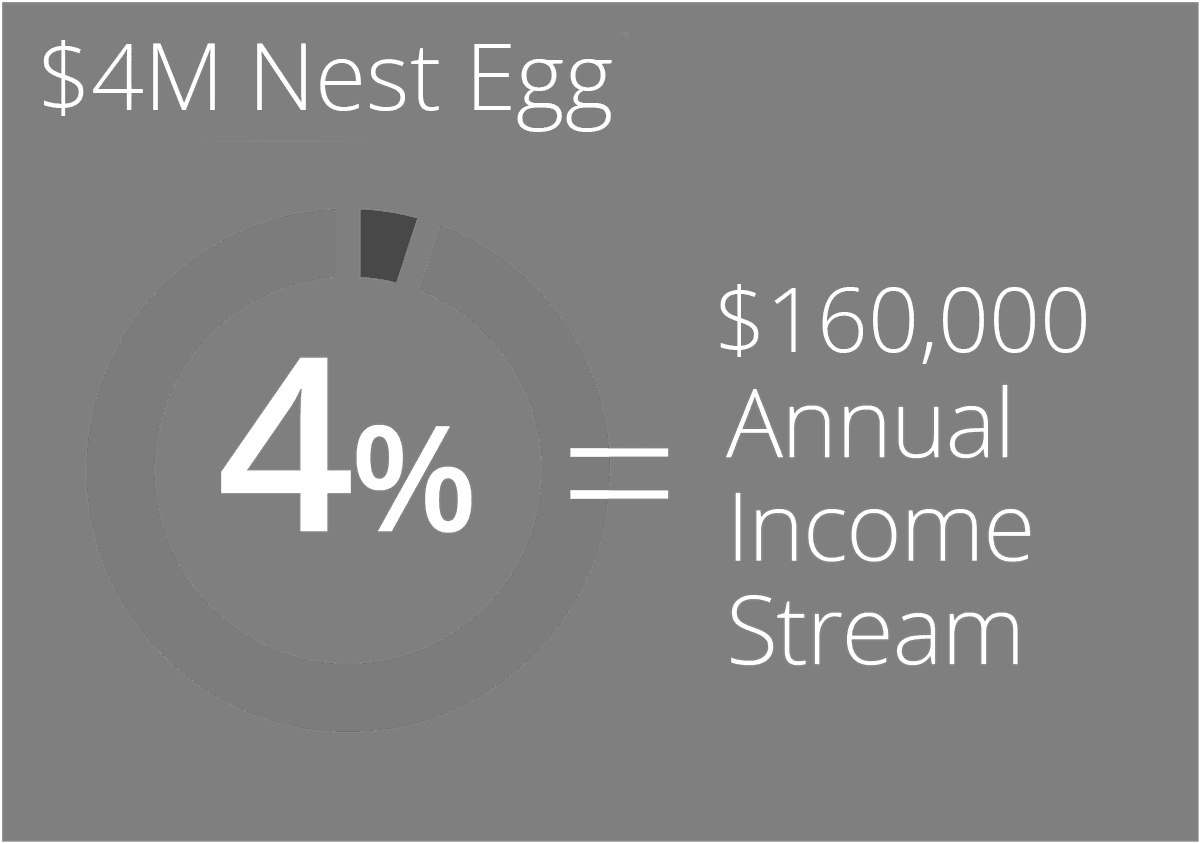

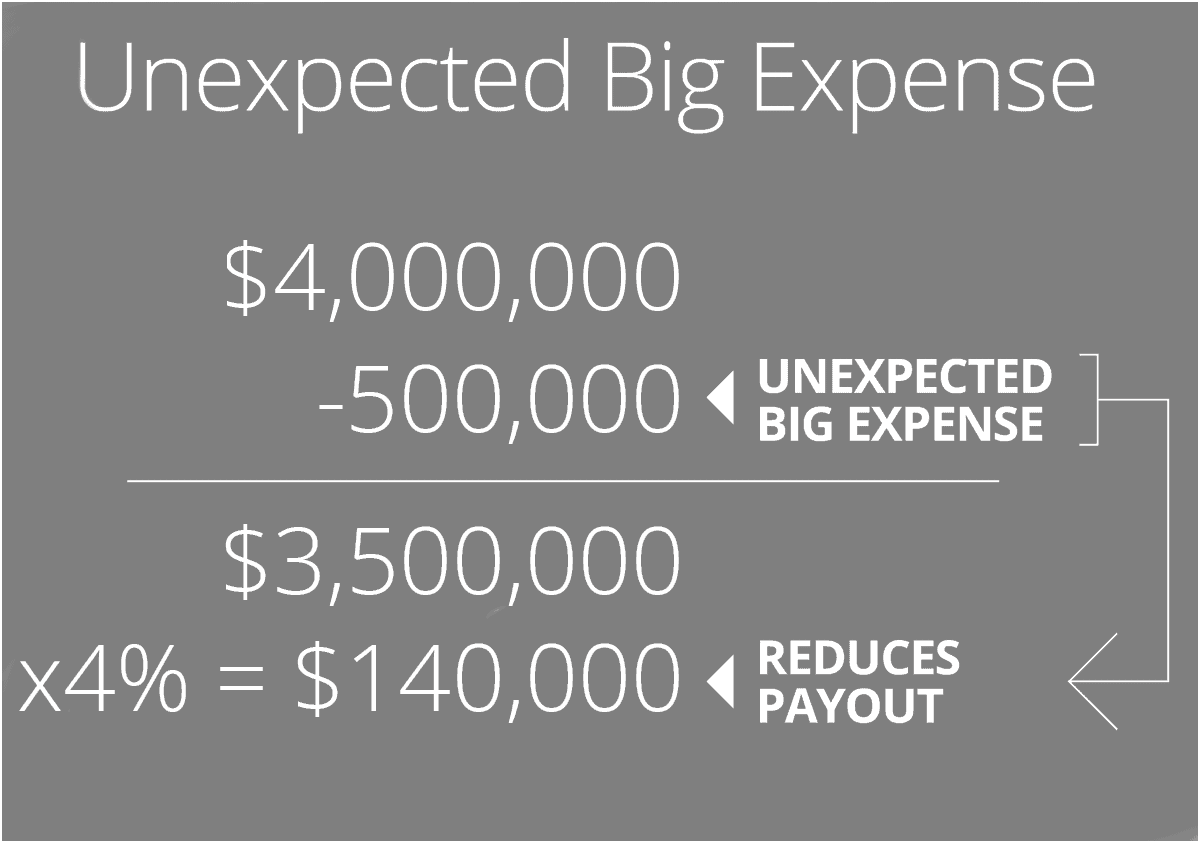

Say you have a $4 million nest egg. You decide to withdraw a 4% income stream from your nest egg every year to live the lifestyle you desire.

After a year, say a large unexpected expense comes up. Now you need to withdraw an additional $500,000 cash beyond your monthly income. This brings your nest egg’s relative value down to $3,500,000, reducing your yearly payout. You just gave yourself a pay cut in retirement. That’s the last thing you want to do—especially since inflation increases the cost of living during your 20–30 years of retirement.

A Raise in Retirement? Here’s How Our Strategy Can Make That Possible

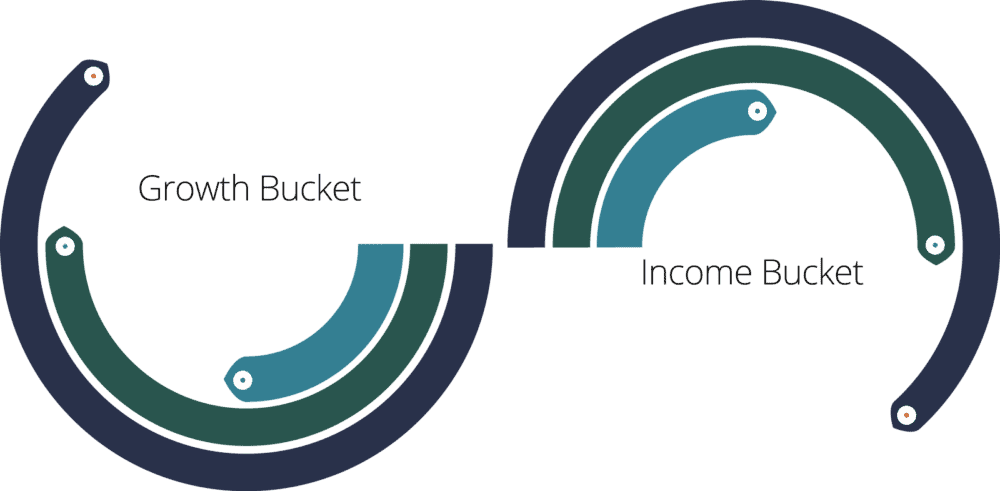

To address these challenges, we divide your nest egg into two buckets.

Income Bucket: Stability and Income Generation

Money to draw income from during retirement. Since you rely on this money to live your life, it’s invested in moderately conservative allocations. This bucket can provide a reliable stream of income to meet your needs, regardless of market conditions.

Growth Bucket: Long-Term Growth Potential

Money set aside to grow through bolder allocations. Moving gains into the Income bucket can help preserve them. We design these portfolios to leverage market opportunities while managing downside risk, allowing for regular growth over time.

Dividing your nest egg into these buckets helps accomplish several significant things:

1. Withdrawing money from the Growth bucket for unexpected expenses leaves your income stream unaffected.

2. Gains earned in the higher-risk Growth bucket can be moved into the more conservative Income bucket to help preserve those gains.

3. Shifting gains from Growth to Income increases the Income bucket’s bottom line. You just gave yourself a raise!

Helping To Preserve Your Nest Egg

Your nest egg is critical, and helping preserve it through unforeseen expenses or market volatility is an important priority. We help implement risk management techniques designed to help preserve your retirement savings, so you’re better prepared for whatever the future may bring.

Case Studies: Real-World Success Stories

Growing Wealth in Retirement

One of our clients, a Chicago-based retiree, transitioned to a retirement lifestyle with the help of our investment strategies. With our tailored portfolio and income-generating assets, they were able to preserve their wealth and enjoy financial security throughout retirement.

Understanding investments through divorce:

Navigating Market Volatility

A client in Milwaukee, WI, turned to us when market volatility threatened their investment goals. By actively adjusting their portfolio and managing risk, we helped them weather the downturn and emerge stronger, preserving their assets.

Expanding Our Reach: Geo-Specific Investment and Wealth Management

We understand that each region has its unique financial landscape. Our firm provides tailored wealth management services in various locations, ensuring that clients in different areas receive strategies suited to their economic conditions.

- Wealth Management in Madison, WI

- Wealth Management in Milwaukee, WI

- Wealth Management in Clearwater, FL

- Wealth Management in Palm Harbor, FL

- Wealth Management in Lake Geneva, WI

Insights & Resources

Stay informed and up-to-date with our insights into the financial world.

- Market Commentary

Regular updates on market trends and analysis to help you make informed decisions. - Investment Strategies

Insightful breakdowns of successful strategies for growth, income, and retirement. - Financial Planning Tips

Practical advice to keep your financial goals on track.

FAQs About Legacy Financial Planning

Investment management focuses on asset growth through strategic investments, while wealth management includes estate planning, tax strategy, and broader financial planning.

Look for a firm with a strong track record and ability to tailor strategies to your needs.

Use tax-efficient investing techniques, including tax-deferred accounts and tax-loss harvesting.

Balance income-generating and growth-oriented assets with diversification and strong risk management.

Through dynamic risk management strategies and diversified portfolio structures.

It helps to ensure that all investment strategies align with your life goals and changing needs.

Consider estate planning, charitable trusts, and tax-efficient portfolios tailored to long-term goals.

We tailor plans based on each region’s economic conditions and financial opportunities.

Learn more about investment strategies that help grow your wealth during retirement in our book Sunny Side Up. We’re here to guide your lifelong journey of financial success.

See how we can help you invest smarter to reach your ideal financial life faster.